The lingering energy shock is morphing from the Asian epicenter to a global economic drag. The U

When the U

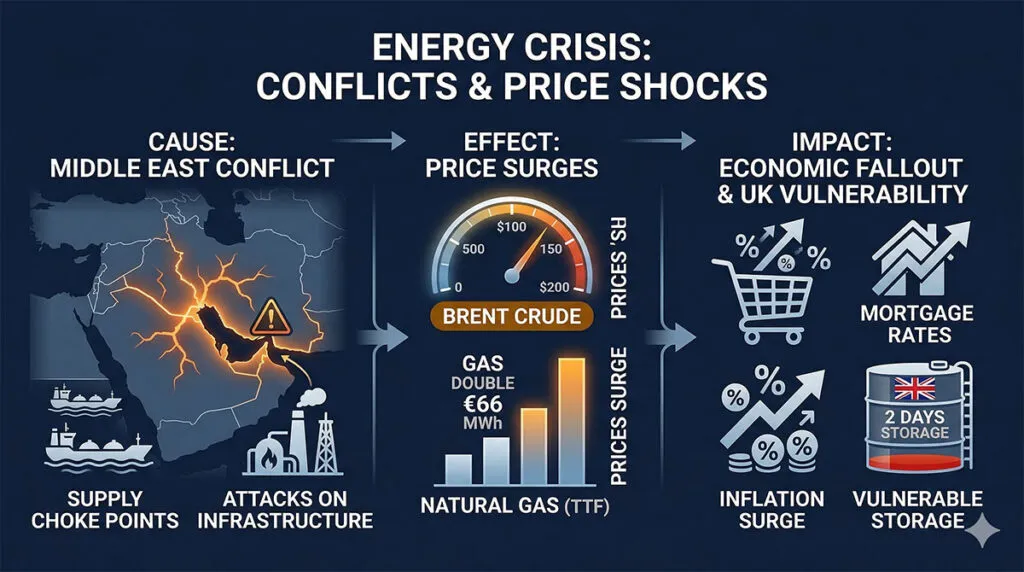

But the real danger was never confined to crude oil. The crisis has evolved into a broader energy, logistics, fertilizer, food and financial shock.

What began as a regional conflict has become a structural drag on the global economy.

Prolonged pain

Recent warnings by the International Energy Agency (IEA), the International Monetary Fund (IMF) and the World Bank underscore the same point.

Even if military hostilities continue to ease, energy systems, shipping networks and commodity supply chains will require many months—and in some cases years—to normalize. The result is likely to be a weaker global economy in the second half of 2026 and throughout 2027.

FIG1: Global Energy Shock Impact Trends 2026 H2 - 2027

Sources: IEA, IMF WEO, World Bank, Reuters, author’s assessment

The core issue is persistence. The IMF warns that prolonged energy disruptions could push the world toward recessionary conditions. The World Bank expects rising energy prices in 2026, while the IEA reports tightening supplies, falling inventories and continuing refinery disruptions.

The world faces a prolonged period of elevated energy costs, fragmented trade routes, higher insurance premiums, supply-chain restructuring and slower productivity growth.

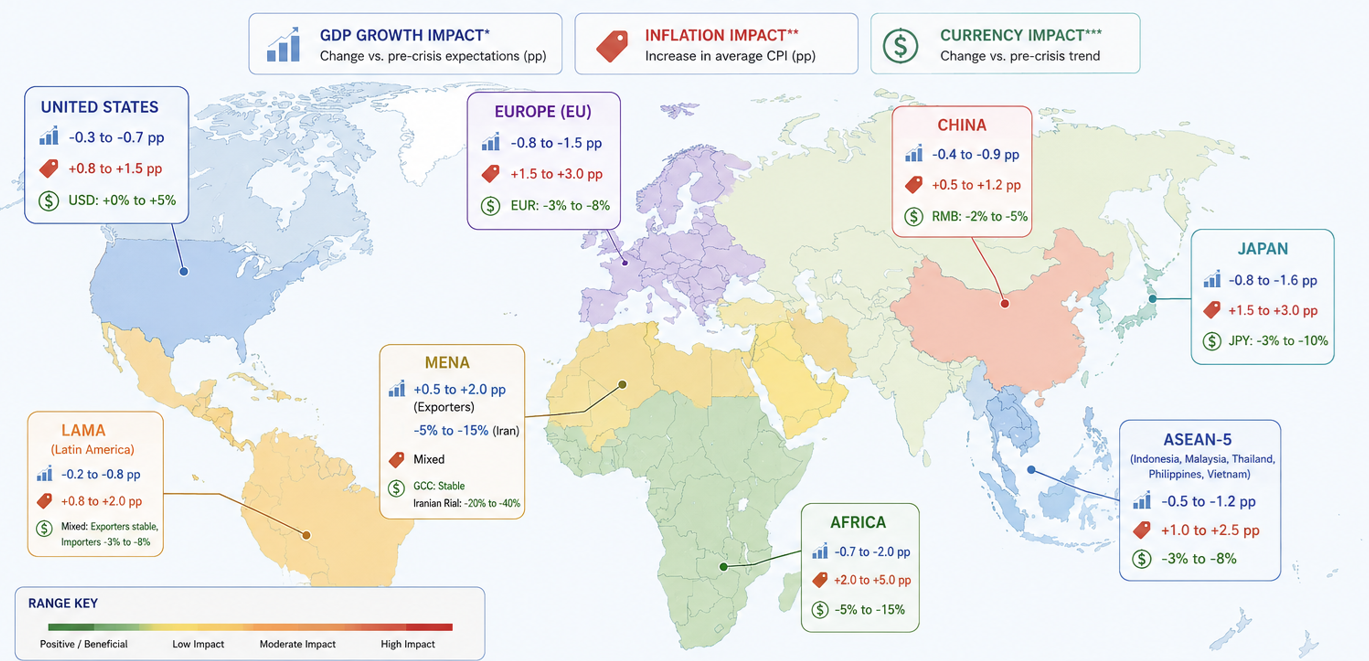

U.S.: Resilient but increasingly stagflationary

The United States is better positioned than most advanced economies because of domestic energy production and continued AI-led investment. Yet, higher fuel, petrochemical and transport costs are already feeding through the economy.

Gasoline prices remain well above pre-war levels, while energy-intensive industries face sustained cost pressures.

Growth is likely to remain positive through 2027, but below pre-conflict expectations. Inflation may prove more persistent than policymakers anticipated.

The principal risk is not recession but a stagflationary environment characterized by slower growth, elevated prices and tighter financial conditions.

By targeting Iran's strategic capabilities while expanding military deployments across the region, the U.S. has contributed to a prolonged risk premium in global energy markets.

At the same time, it has left Europe, Japan, South Korea and much of the developing world highly vulnerable to the resulting energy shock.

China: Economic exposure, strategic beneficiary

As the world's largest energy importer, Beijing remains vulnerable to disruptions in Gulf oil and LNG supplies. Higher energy prices, weaker external demand and increased transport costs will likely moderate Chinese growth through 2027.

But Beijing has spent more than a decade preparing for precisely such contingencies. Diversified energy imports from Russia, Central Asia and Africa, extensive strategic petroleum reserves, large-scale renewable investments and expanding regional trade networks provide buffers unavailable to most Asian economies.

More importantly, the crisis reinforces China's long-standing argument that excessive dependence on Western-dominated maritime routes and financial systems constitutes a strategic vulnerability.

As Gulf states, Asian economies and many Global South nations seek greater economic resilience, China is positioned to benefit through expanded infrastructure investment, energy partnerships and trade integration.

The United States remains the predominant military actor in the crisis, but China is emerging as one of its principal geopolitical beneficiaries.

Europe: The most vulnerable advanced region

Europe remains the weakest link among advanced economies. The continent has not fully recovered from the energy consequences of the Ukraine conflict.

The Iran-related shock has compounded existing vulnerabilities by raising LNG competition, industrial costs and fertilizer prices.

Germany illustrates the challenge. Its manufacturing sector faces a second major energy shock within five years. Industrial competitiveness is likely to deteriorate further, while fiscal constraints limit governments' ability to cushion households and firms.

Southern Europe may perform somewhat better due to tourism, but energy costs will continue to restrain investment.

For Europe as a whole, 2027 may bring stagnation rather than recession. Yet stagnation itself represents a significant deterioration relative to earlier expectations.

European geopolitics revolves around an imagined Russian attack, yet the region’s economic fundamentals are being undermined by the protracted energy shock.

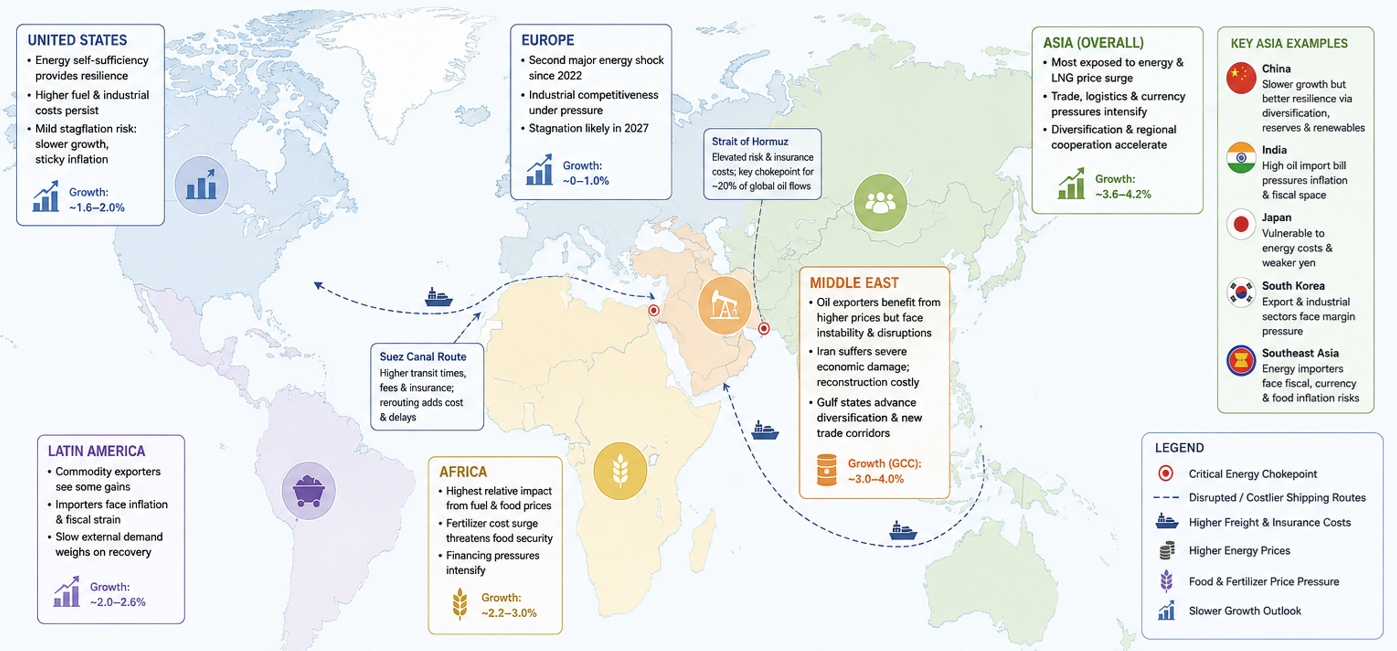

Asia: Still the epicenter

Asia remains the region most exposed to the lingering crisis. The transmission mechanisms identified earlier—oil, LNG, trade logistics and financial spillovers—have intensified rather than disappeared.

The most vulnerable major economies are Japan, South Korea, India and many Southeast Asian importers. All depend heavily on imported hydrocarbons. Higher energy bills worsen trade balances, pressure currencies and reduce household purchasing power.

India faces a more difficult balancing act. Strong domestic demand and favorable demographics remain strengths, yet sustained oil prices near or above $90 per barrel would raise inflation and fiscal pressures. The country's growth rate will likely remain among the world's highest, but below its potential.

Across Asia, the crisis is reinforcing long-term trends toward energy diversification, regional trade arrangements and reduced dependence on vulnerable maritime chokepoints.

Middle East: Huge structural damage

In the Middle East, oil-exporting states benefit from higher prices but suffer from geopolitical instability and disrupted export routes.

The Gulf monarchies—particularly Saudi Arabia, the UAE and Qatar—possess financial buffers that allow them to absorb short-term volatility. Yet, infrastructure damage, shipping disruptions and investment uncertainty are imposing significant costs. Full normalization of regional energy logistics could take years.

Iran remains the principal economic casualty. Even if hostilities diminish, sanctions, damaged infrastructure and capital flight will weigh on growth for years. Reconstruction needs will be immense.

The broader regional consequence is the acceleration of economic diversification. Gulf states will intensify efforts to reduce dependence on hydrocarbon exports, while simultaneously investing in alternative trade corridors and logistics networks.

Since fall 2023, a set of unwarranted wars in the Middle East has severely penalized the colossal modernization initiatives in the Gulf.

Latin America: Mixed effects, darkening skies

Latin America faces a divided outlook. Commodity exporters such as Brazil benefit from higher agricultural and resource prices. Yet gains are partly offset by weaker global demand and tighter financial conditions.

Mexico faces indirect exposure through slower U.S. growth and manufacturing demand. Argentina illustrates the vulnerability of heavily indebted economies. Higher energy costs and global financing pressures complicate stabilization efforts.

More broadly, countries with large fuel-import bills will face renewed inflationary pressures.

Overall, Latin America is unlikely to experience a major crisis, but the region's recovery trajectory will slow amid darkening skies. It is the target of the Trump administration’s lethal imperial dreams – from Panama, Venezuela, Cuba and Nicaragua to Argentina, even Colombia.

Africa: The disproportionate victim

Africa may suffer the greatest relative damage. The World Bank and IMF have repeatedly warned that poorer economies bear a disproportionate burden from higher fuel and fertilizer costs.

For many African countries, the energy shock rapidly becomes a food-security shock. Rising transport, fertilizer and import costs feed directly into consumer prices and poverty rates. Countries such as Egypt, Kenya and Senegal face growing external financing pressures.

Even resource exporters like Nigeria and Angola confront governance and investment challenges that limit the benefits of higher oil prices.

The most concerning issue is food security. There are deep interconnected vulnerabilities linking natural gas, fertilizer production and agricultural output. The consequences could extend well beyond 2027.

Global outlook through 2027

The most likely outcome is neither global recession nor rapid recovery. Instead, the world appears headed toward a prolonged adjustment period characterized by Brent crude averaging roughly $85–100 per barrel, plus persistently elevated LNG and shipping costs.

These translate to higher food and fertilizer prices, slower global trade growth, renewed inflationary pressures and lower business investment due to uncertainty.

FIG2: Persistent Disruption Impact

Sources: IEA, IMF WEO, World Bank, national sources, author’s assessment

Under this baseline, global growth is likely to remain near or in the proximity of 2.8–3.1% through 2027; below pre-conflict expectations but above outright recession levels.

The principal danger lies in a prolonged energy disruption or renewed military escalation, which could push oil prices toward the $110–125 range envisioned in adverse IMF scenarios and substantially increase recession risks. The era of relatively cheap, secure and politically predictable energy flows is fading.

What is emerging instead is a more regionalized, more expensive and more geopolitically contested energy system—one whose economic consequences will extend well beyond the battlefield and well beyond 2027.