The U.S./Iran-linked energy crisis has shifted from a commodity shock to structural geopolitics, with Asia at the epicenter due to its dependence on imported oil and LNG. Global reverberations can no longer be avoided.

(Credit: Fox News)

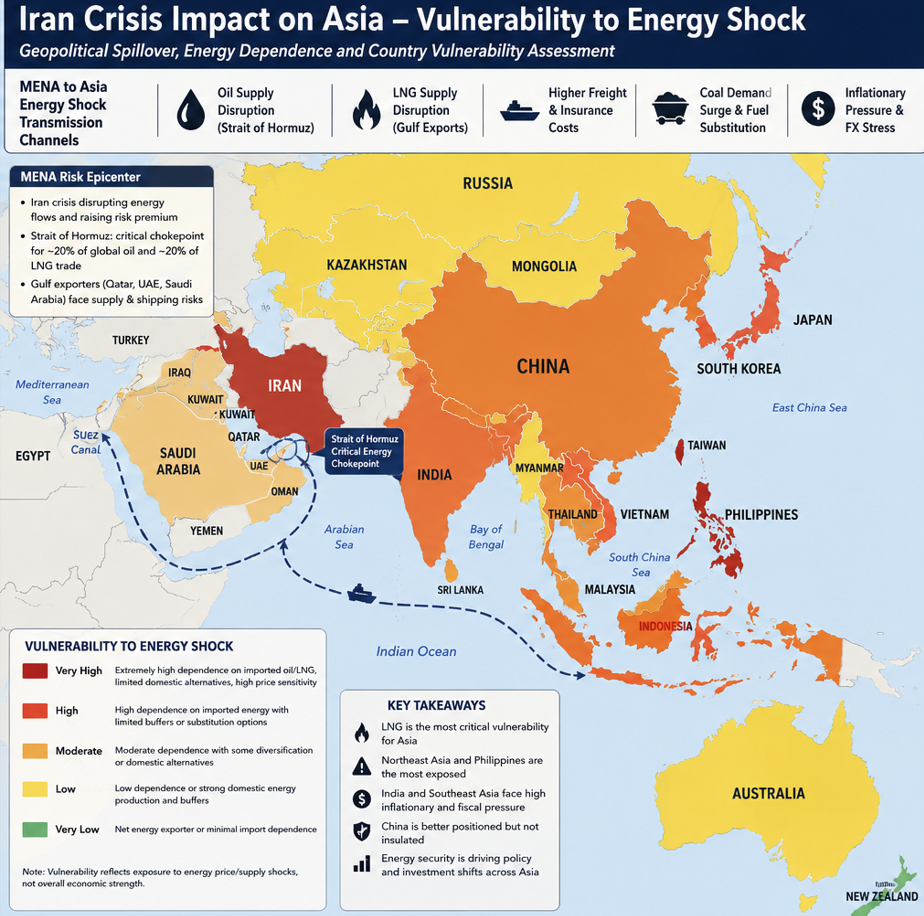

In the Asian shock, four transmission channels play a role. In the case of oil, elevated risk premium is coupled with physical tightening via Strait of Hormuz disruptions.

Liquefied natural gas (LNG) poses a more severe constraint than oil and thus structural tightening of Asian gas balances. Meanwhile, coal substitution is experiencing a short-term demand surge in Asia, especially in India, China and Southeast Asia.

On the economic side, countries are struggling with imported inflation, foreign exchange pressure, and painful policy trade-offs between subsidy support and fiscal stability.

The shock is no longer a temporary price spike but a sustained supply reordering. The International Energy Agency (IEA) projects large-scale oil drawdowns. LNG disruptions are removing 20% of global LNG flows at peak disruption, which will tighten Asian supply chains significantly.

What happens in Asia won’t stay in Asia. In the coming months, the adverse reverberations will be felt across the world.

Asian Century and global growth at stake

Asia remains the engine of global economic growth, with China and India alone contributing roughly 40–45% of incremental global GDP growth, while other major Asian economies—Indonesia, South Korea, Vietnam, and ASEAN collectively—add another 10–12%.

In the medium term, Asia’s share of global growth is expected to rise further as Western economies slow, driven by demographic momentum, urbanization, and productivity gains in services and manufacturing.

However, a severe energy crisis, particularly if it triggers sustained LNG and oil shortages, would sharply compress industrial output, inflation-adjusted consumption, and investment in these economies, potentially reducing global growth by 1–2 percentage points in 2026–27.

An Asian slowdown would have significant spillovers to the U.S., Europe, and Japan through trade, investment, and financial channels. Reduced Asian demand would depress exports of machinery, electronics, and consumer goods from these regions. Higher energy prices would further weigh on consumption and industrial costs. Financial markets could face increased volatility, amplifying capital flow disruptions.

In Japan, the combination of energy dependence and weaker regional demand could sharply constrain growth, while Europe and the U.S. would experience slower industrial output and dampened inflation-adjusted consumption, reinforcing the global drag from the Asian energy shock.

Oil tightness, LNG constraint, brief coal rebound

Oil remains volatile but more flexible than gas. Prices surged above $100/bbl during peak disruption and remain elevated ($90–100 volatility band in stress conditions).

Strait of Hormuz instability has removed millions of barrels/day of export capacity. OPEC+ spare capacity is partially offsetting but insufficient to normalize inventories. Inventories are falling at record pace, reducing the buffer against further shocks.

Unlike earlier cyclical oil shocks, this episode is characterized by structural inventory depletion, making price spikes more persistent even if supply partially recovers.

Nonetheless, natural gas is the primary stress point for Asia. Up to 20% of global LNG supply was disrupted at peak due to Hormuz-linked flows. Asian LNG prices surged above $20/MMBtu in multiple spot windows.

Northeast Asian importers (Japan, Korea, China, Taiwan) entered emergency procurement and rationing. Long-term contracts are under stress due to force majeure risks and shipping rerouting constraints.

Asian LNG imports have dropped sharply. Qatar/UAE-linked exports remain vulnerable due to chokepoint exposure. LNG is increasingly perceived in Asia as less reliable as a transition fuel, accelerating diversification away from gas-heavy strategies in parts of the region.

Then there is the curious rebound of coal, temporarily distorting markets. Asia’s immediate adjustment has been substitution, not demand destruction. China, India, Indonesia and other countries have increased coal burn in power generation. In several ASEAN economies, this is increasingly seen as short-cycle substitution, not structural reversal.

Renewables deployment acceleration continues in parallel (especially China, India).

How are countries coping

China is managing a dual challenge: LNG exposure plus industrial cost pressure. Hence, the simultaneous deployment of coal and renewables. Strategic LNG diversification has increased from the Middle East to Russia, U.S. and Australia. Energy security is now embedded into industrial policy response.

India is highly exposed to imported LNG and oil inflation. A strong coal buffer limits crisis severity but increases environmental cost, which is already soaring with the nation's broad takeoff. Unsurprisingly, fiscal pressure is rising from fuel subsidies. The net effect is manageable but inflationary growth drags.

Japan and South Korea are structurally most exposed to LNG disruption. So, emergency procurement and demand management measures have been activated, with the acceleration of nuclear restarts and efficiency gains. Now energy security dominates macro policy debate.

Southeast Asia (Indonesia, Vietnam, Thailand, Philippines) is highly price-sensitive to LNG demand. Consequently, LNG project cancellations and delays have a painful impact, which is rapidly translating to political volatility. Hence, the efforts to re-optimize coal in Indonesia and Vietnam.

Longer-term shift prevails toward renewables and regional grid integration. But as energy reserves are diminishing, the focus is on the short-term. To paraphrase Keynes: in the long-run, we're all dead.

From economic transmission to energy shift

The energy shock is feeding directly into the consumer price index (CPI) via fuel, logistics, and fertilizers. Hence, the secondary pass-through into food prices, notably in South Asia.

Foreign exchange is under severe pressure as import-dependent Asian economies are facing severe currency depreciation pressure. Before the crisis, the U.S. dollar was less than 58 Philippine peso; now, close to 62. Meanwhile, central banks are forced into a tighter-than-expected monetary policy stance.

Industrial slowdown risk is increasing. Energy-intensive manufacturing margins are compressed. Fertilizer, petrochemicals, and steel sectors are most exposed.

The crisis is accelerating three structural shifts. The first entails the move from LNG expansion to LNG risk hedging.

Second, the past objective to move away from fossil transition has been superseded by energy security primacy.

Third, electrification has accelerated. Renewables and storage investment are front-loaded. The future is not next year. It's now.

Trump–Xi Summit: hope for stability

Prior to Presidents Xi Jinping and Donald Trump meeting in Beijing, analysts hoped that the U.S.-China talks could serve as a stabilizing variable for global energy markets in three ways.

Strategic signaling fosters oil price stabilization, just as U.S.–China coordination reduces demand-side geopolitical uncertainty. The potential easing of tariff and geoeconomic tensions could support global demand expectations.

Second, LNG trade realignment suggests that China may diversify LNG imports further from politically sensitive corridors. U.S. LNG exports could benefit from strategic trade normalization, while Europe–Asia LNG competition could moderate if U.S.-China trade improves.

Third, there is the political minefield of sanctions and Iran-related diplomacy: Even limited coordination could reduce escalation probability in the Middle East, which is vital to avoid extreme oil price spikes.

From the standpoint of the energy markets, the Summit was less about immediate supply restoration and more about reducing geopolitical volatility embedded in energy pricing. But the success of the Summit will be determined by the markets only in its aftermath.

Unsettling scenarios for 2026–27

Base scenario: Partial stabilization of the Middle East conflict proceeds without full resolution. Hormuz remains intermittently disrupted but not fully closed. LNG supply is partially restored but tight. Oil inventories rebuild slowly but remain below norm. Brent crude varies around $85–105/bbl and LNG Asia spot at $12–20/MMBtu. Inflation stays elevated but manageable. Asia faces growth drag but no recession.

Optimistic scenario: Diplomatic stabilization is supported by U.S.–China coordination following the Summit. Shipping lines are gradually reopened. LNG infrastructure is partially restored. OPEC+ increases output into recovering demand. Brent crude falls to $65–85/bbl and LNG to $8–14/MMBtu. Inflation falls sharply in Asia. Policy easing resumes globally and energy transition investments accelerate again.

Pessimistic scenario: Renewed military escalation takes off in the Iran–Gulf theater. Hormuz's closure is sustained or repeated. LNG infrastructure damage spills over in Qatar/Gulf. Severe inventory depletion triggers panic buying. Brent crude soars to $110–140+/bbl and LNG climbs to $20–35/MMBtu. Severe imported inflation shock spreads, with industrial slowdown and rationing risk in parts of Northeast Asia. Renewables and coal substitution surge simultaneously. With financial volatility, emerging market currencies fall and capital flight resumes.

The 2026–27 outlook is at best clouded in uncertainty. The concern is that it will morph into high plateau volatility.