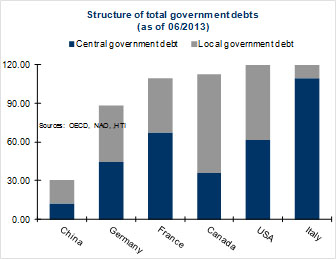

The rapidly swelling local government debt in China over the past few years are seen by many as a trigger to a credit bubble, or even full-blown financial crisis. China’s local government debt to GDP ratio expanded to 31.5% by June 2013, according to the National Audit Office, and continued to climb to 33.8% by 2014, according to our estimates. Over 50% of new borrowings have been used for repayments since 2014, signaling significant repayment pressure.

Policy mix to curb local government debt

Budget reform, the first critical reform among over 330 reform proposals of Xi administration, has kicked off, laying the foundation for a more balanced and transparent government budget and financing structure. New Budget Law, regarded as “Economic Constitution”, was approved on August 31 of 2014 and launched on January 1 of 2015, after a decade of amendments and negotiations. The debt issue was also a focus on the recent Two Sessions for March 3-15 of 2015. Lou, Minister of Finance, summarized the key solution to local government debts as “opening the front gate and closing the back door.” In other words, the central government is to leave more flexibility for local governments including municipal bond issuance, while closing other non-transparent channels such as Local Government Financing Vehicles (LGFVs) and bank loans.

Lou also stated that a RMB 600 bn quota was approved for new bond issuance including RMB 500 bn general bonds and RMB 100 bn special bonds in 2015; a swap plan of RMB 3 tn in total was announced to roll over existing LGFVs, 1 tn of which has been allocated to local governments by the MoF based on their maturing outstanding debts and affordability. The plan includes issuance of low-cost long-term local government bonds, whose proceeds are used to repay high-interest short-term bank loans, local investment bonds and trusts. According to the MoF, the swap plan can reduce annual interest payments by RMB 40-50 bn, largely easing local governments’ repayment pressure.

The short-term crunch could be partly alleviated via the debt swap plan and new municipal bond issuance, but there remains a long way to achieve the spirit of the new Budget Law. Related financial, fiscal and legal reforms are required to improve the fiscal position of local governments fundamentally. Short term measures include:

- Deleverage below a clearly defined cap of the debt/GDP ratio within an explicit time-table. A range of 30-40% of GDP could be a feasible working zone for local governments, and an explicit timetable to deleverage is equally important. Highly indebted local governments should be requested to deleverage via selling government owned assets, securitizing debts, and getting a clean slate from the central government.

- Bailout fund urgently needed in case of debt crisis. It would be mainly used to bailout problematic local governments, led by a unified regulatory body. The fund could be raised from various channels including fiscal revenues, tax transfers, sales of state-owned assets and PBOC loans.

Solutions for a longer term are required for a more sustainable and transparent government financing structure. Major measures include as follows:

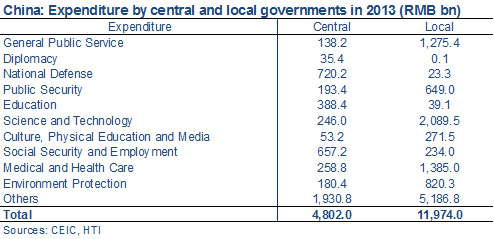

- Rebalance local government spending to reflect tax revenues. The central and local governments share tax revenues 50/50, but the spending proportion is roughly 30/70.Shifting more expenditure responsibilities to the central government is in progress, especially in the field of public security, education, environment protection, and medical and health care.

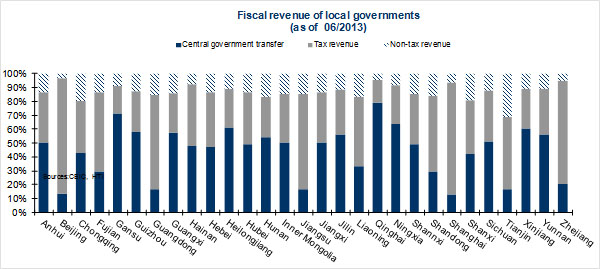

- Give local governments certain flexibility in local taxes. Besides municipal bond issuance, it is critical to levy property tax as a stable long term revenue source, allow local governments to develop local taxes to meet local needs, and improve the central government transfer system in a more regulated, transparent and fair way.

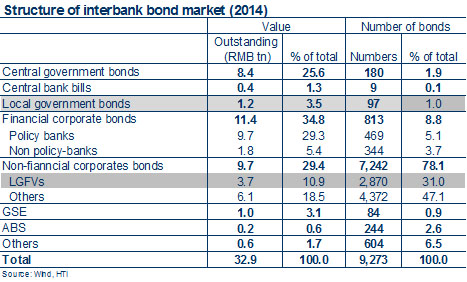

- Unify regulatory bodies and strengthen supervisory and monitory systems. Multiple regulators including the MoF, PBOC, CDRC and CSRC exist for different types of bonds issued and traded in China, which jointly form fragmented markets with different rules and standards. A unified regulatory body is urgently called for an integrated market, supervised by a comprehensive system, with requirements on transparent information disclosure.

- Promote an effective market mechanism. China’s bond market, despite the third largest in the world, is highly illiquid and inefficient in terms of participation and pricing mechanism. Soft budgets led to over investment and overspending, which should be changed to hard constraints to oblige local governments to reduce or cease financing activities whenever they are out of money. Credit rating agencies need function in a more independent, fair and competitive way.