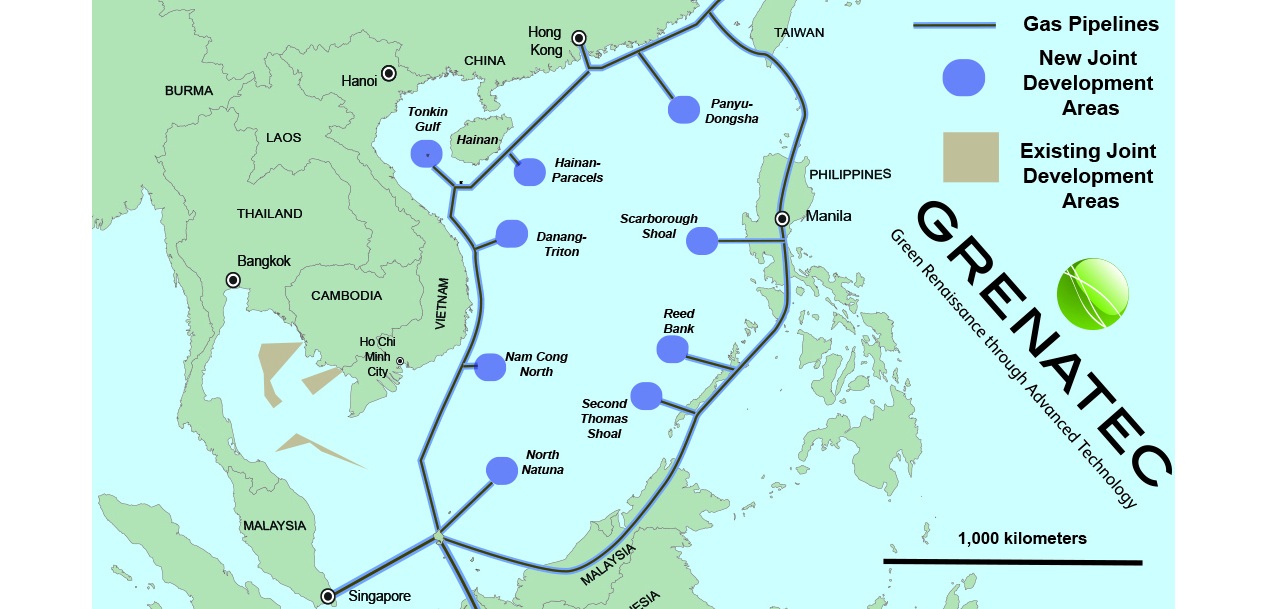

Multilateral South China Sea energy infrastructure connected to offshore Joint Development Areas (JDAs) offers an attractive solution to territorial tensions.

Such a flexible, adaptable, ‘future proof’ Pan-Asian Energy Infrastructure could serve Asia for a century or more. It would dramatically reduce Asian carbon emissions.

The positive implications of thinking big, thinking multilaterally and thinking long-term about energy security, energy market reform and large-scale carbon emission reduction are hard to overstate.

That’s because rising territorial tensions in the South China represent a classic economics case of the ‘Tragedy of the Commons.’ This occurs when ambiguous resource property rights create an incentive for aggressive, environmentally unsustainable exploitation by the nimble. The reason: delay leads to sharing.

China’s nine-dotted line, China’s placement of an ‘exploratory’ oil rig in waters claimed by Vietnam and recent statements by Chinese energy giant CNOOC Group it may deploy Floating Liquid Natural Gas (FLNG) technology in other disputed South China Sea areas can all be seen as a logical ‘first mover’ strategy to take advantage of a ‘tragedy of the commons’ situation.

Joint Development Areas (JDAs) have been around since the 1960s. They exist all over the world. Under JDAs, countries with conflicting offshore territorial claims agree to postpone resolution of the claims while they cooperate to develop the resources within them.

Two JDAs already exist in the South China Sea. The Tonkin Gulf, lying between North Vietnam and China’s Hainan Island, is an ideal location for a third.

There, China and Vietnam are already engaging in joint offshore exploration. Should developable resources be found, China and Vietnam could jointly develop these under a JDA. This could set a precedent for others off central and southern Vietnam, Malaysia, the Philippines and even southern China. Consortia of companies would develop the projects, spreading investment risks.

At present, offshore gas field investment is almost always funded by multi-decade contracts between buyers and sellers. But these are based upon little more than guesses where long-term prices may go. The results can be gluts, shortages and volatile spot prices as such guesses diverge from reality. This benefits only speculators — a sign of market ill health. By contrast, more liquid and responsive markets enabled by a network architecture can help supply and demand stay in better sync, creating more predictable pricing.

A strong argument can be made that participating in multilaterally auctioned JDAs/MDAs in the South China Sea where proceeds are recycled into infrastructure offers China greater opportunities than aggressive unilateral development.

The reason is that China’s state champion oil and gas companies (such as CNOOC and Petrochina), gas pipeline construction companies and electricity infrastructure companies (such as State Grid Corp of China and China Southern Power Grid Company) are almost certain to be prime beneficiaries.

One can easily argue China’s motivation for creating its proposed $100 billion Asian Infrastructure Investment Bank (AIIB) was to recycle her multi-trillion trade surpluses into offshore infrastructure opportunities for her state champions.

That’s because these companies face atrophy without new projects as China’s internal infrastructure needs are increasingly met.

Handled right, this international re-orientation of China’s infrastructure-building industry can benefit everyone. The key is to ensure such infrastructure is built and operated on an ‘open access, common carrier’ basis, open to everyone and immune from political decision-making. This shouldn’t be controversial. China is already applying such reforms to its internal market. Applying it externally enhances market consistency.

Southeast Asia’s centrally-located, energy trading city state of Singapore is ideally suited to playing the ‘honest broker’ in managing a multilateral South China Sea energy infrastructure. Singapore’s already slated to play a major role in ASEAN’s proposed Trans-Asian Gas Pipeline (TAGP) and Trans-ASEAN Electricity Grid (TAEG). These are Southeast Asia’s two regional templates that could serve as the core of a Pan-Asian Energy Infrastructure.

Later this year, China hosts meetings of the Asia Pacific Economic Cooperation Group. China has indicated it wants infrastructure and deeper regional economic integration to be among chief topics of discussion. Later, Australia will host the annual meeting of the Group of 20 largest economies. Australia similarly wants infrastructure investment on the agenda.

APEC and the G20 offer the perfect opportunity to discuss the deeper multilateral energy networks of tomorrow and the economic benefits they can provide. This could enhance recognition of the role efficient multilateral energy infrastructure can play in reducing climate change – a key agenda item at next year’s crucial COP21 meeting in Paris.

Stewart Taggart, a former financial journalist, is founder and principal of Grenatec, a Sydney, Australia-based non-profit research organization studying the viability of a Pan-Asian Energy Infrastructure.

Wu Zurong Research Fellow, China Foundation for Int'l Studies

Wu Zurong Research Fellow, China Foundation for Int'l Studies Philip Cunningham Visiting research fellow, Cornell University, New York

Philip Cunningham Visiting research fellow, Cornell University, New York Yang Li Deputy Director at the Research Center for Oceans Law and Policy

Yang Li Deputy Director at the Research Center for Oceans Law and Policy Richard Javad Heydarian author of "Asia's New Battlefield: US, China, and the Struggle for Western Pacific"

Richard Javad Heydarian author of "Asia's New Battlefield: US, China, and the Struggle for Western Pacific"- Richard Javad Heydarian author of "Asia's New Battlefield: US, China, and the Struggle for Western Pacific"