Cars await loading onto a ship for export at Yantai Port in east China’s Shangdong Province on May 9, 2023. According to KPMG, Chinese car brands accounted for less than 10 per cent of the 1.1 million battery-powered EVs sold in Europe in 2022. (Photo: Xinhua)

Today, the EV industry serves as a pivotal element in the renewable transition and green energy strategies of major international players, rendering it both strategically contested and geopolitically significant.

Over the past fifteen years, the global automotive industry’s sector witnessed a seismic transformation, given China’s meteoric rise as a powerhouse in the electric vehicles (EV) market – surpassing Japan, Europe, and the United States and establishing itself as the world’s largest EV manufacturer. With a combination of state-driven, top-down industrial policymaking and the ensuing pivoting of private capital and investment, the Chinese economy has seen a rapid uptake in the production of budget-friendly, high-quality, and cost-effective EVs.

In the meantime, European carmakers are facing increasingly tough competition from China, as they struggle to maintain their foothold in the world’s second largest market. It is hence no surprise that there is a growing chorus of European critics charging that China’s comparative advantage had been secured through protectionist subsidies. A mixture of domestic political apprehensions, coupled with a shifting focus upon ‘de-risking’ Europe’s economic relationship with China, have nudged the EU to take a sterner stance towards the importing of EVs, as well as subsidising domestic and homegrown EV-manufacturing capacities, in attempt to counterbalance China’s astronomical rise.

Wherefore Europe?

As we enter into the 2020s, the global EV industry is witnessing unprecedented uncertainties and turmoil. Geopolitical tensions have begun to cast shadows over the industry at large. During her State of the Union address on September 13th 2023, von der Leyen made a politically significant announcement: the EU was due to conduct a thorough anti-subsidy investigation into Chinese EVs, on grounds of Europe’s commitment to fair competition rather than a “race to the bottom.” This move was purportedly a precursor to the establishment of a mechanism within the EU that would enable to raise supplementary taxes, presently at 10%, to counteract the “artificial” market distortions caused by “huge state subsidies.”

The very decision to drive forward this investigation has received near-unanimous support from key players. Paris and Berlin back this move. France argues that Chinese ‘subsidies’ violate WTO rules, while Germany sees China’s extensive state support for EV production as “unfair competition.” Notably, despite a smaller auto industry compared to Germany, France has actively urged and encouraged the European leadership to adopt the measure. Whilst the ongoing probe’s exact findings have yet to be disclosed, there is a risk that those conducting it are leaning far too heavily into speculation over potential harm rather than established evidence of damage - which may undermine the Commission’s credibility in upcoming lawsuits. European states face risks if China resorts to reciprocal tit-for-tat in view of what it perceives to be provocation on its core economic and strategic interests. Major German car brands heavily rely on the Chinese market, rendering them vulnerable to prospective Chinese retaliation; indeed, Germany’s auto industry contributes up to 10% of its GDP and employs 900,000 workers.

Today, the EU grapples with a critical question: what should its EV manufacturing strategy be? A close and complete alignment with the U.S. appears unlikely, given escalating American protectionism, as illustrated by the Inflation Reduction Act (IRA), and broader concerns that the U.S. remains a self-serving, and fundamentally self-interested power keen on appeasing solely domestic workers and voters who had been purportedly excluded from its globalisation project. A purely ‘de-risking’-oriented approach – whilst potentially effective in seemingly and imminently reducing reliance on both China and the U.S. – may prove to be far too costly and impractical.

The Dangers of Overreaction

European leaders would benefit from first recognising that China’s rise in EV production is by no means inexorable and unassailable. A more prudent approach that is less directly confrontational places greater emphasis upon the development of a parallel competition by pooling private sector resources to develop alternative EV models. This could well suffice as a remedy and response to the ‘China challenge.’ China is not six feet tall – for one, despite becoming the world’s largest EV exporter, has had to deal with dwindling domestic demand, due to economic turbulence unleashed by the COVID-19 pandemic and significant movement restrictions.

Indeed, pragmatism also calls for a level-headed and even-handed assessment of the strengths and weaknesses of China’s EV programme. We must avoid implicitly or indirectly exaggerating the country’s successes. In 2022, China served as the world’s largest EV production hub, accounting for 6.7 million units, constituting 64% of the aggregate global volume. Of these, 580,000 EVs were exported from China, with the majority (407,000) bearing Western brand names. This implies that despite the robust penetration in Europe, Chinese brands have yet to achieve dominance in European markets; China’s market share in Europe, currently around 5%, may reach 9-18% by 2025, impacting domestic sales.

Fundamentally, the EU must recognise that its overall climate aspirations could well be in tension with the relatively trenchant approach championed by some of its bureaucrats on EVs produced and supplied by China. Von der Leyen’s call for the investigation into Chinese EVs is in conflict with three other, fundamental EU objectives: advancing the European Green Deal and continent-wide decarbonisation; promoting climate-friendly mobility, and ensuring affordable, competitive access for European consumers. This is particularly pertinent given the significant 40% price gap between European and Chinese EVs, coupled with the challenges posed by inflation and the sluggish 0.8% Eurozone growth experienced by EU households.

A pragmatic and sensible path ahead involves carefully engaging and working with both China and the U.S. alike for now. The ultimate goals are twofold: first, diversifying beyond these two leading players via consolidating EU’s ties with alternatives such as India and ASEAN countries, and second, ensuring that the EU possesses at least much greater homegrown capacity to design, manufacture, and distribute EVs than in the status quo.

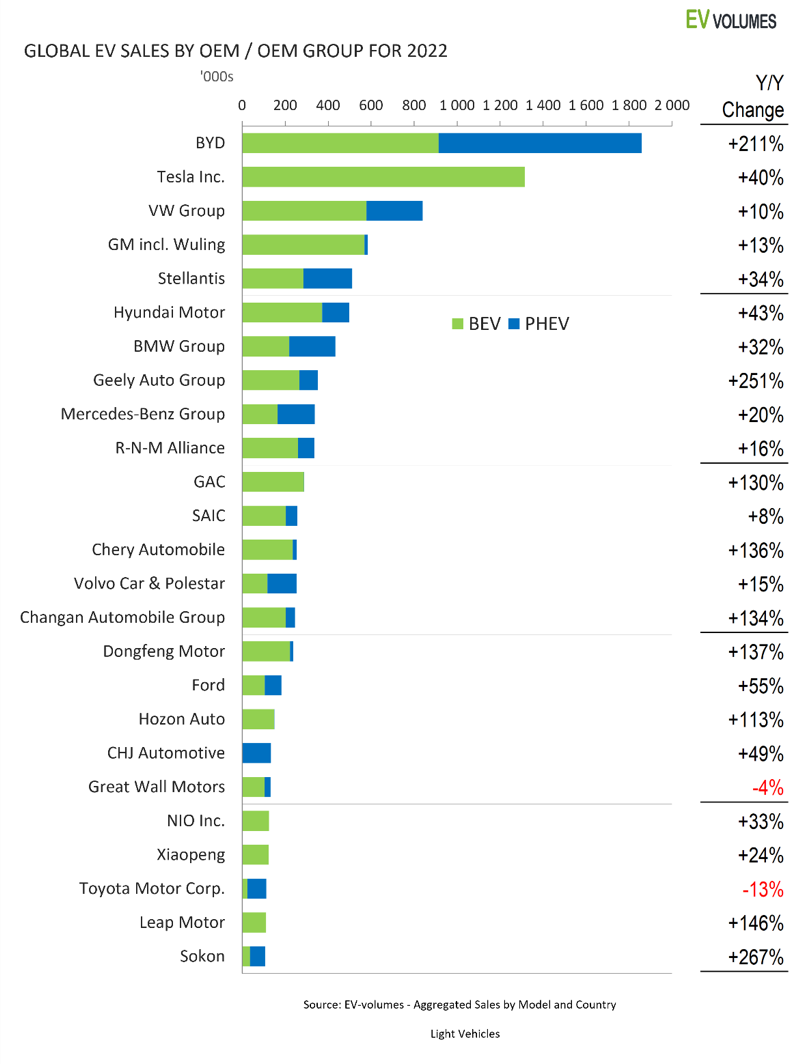

Figure 1. Data supplied by www.ev-volumes.com.

EU leaders must prioritise European interests, not Chinese or American interests.

When read through the lenses of geopolitics and international diplomacy, the EU’s move to investigate and probe Chinese EVs takes on an additional dimension. The Chinese administration is most likely to perceive the measure as a challenge to its sovereignty and interests. Already, its state apparatus has expressed “high concern and strong dissatisfaction,” foreshadowing a potentially downward trajectory in near-time Sino-EU trade relations. Chinese propaganda and media outlets have lambasted the EU’s probe as “naked protectionism” and vow to “firmly safeguard” the interests of Chinese companies.

As argued by economist Alicia Garcia-Herrero, China has a sizeable arsenal of potential tools with which it can signal its reservations, indeed opposition, over the European policy on EVs. Past economic retaliations, as evidenced by Beijing’s reactions to the foreign policy stances of Lithuania in relation to Taiwan, or Australia under Scott Morrison, indicate that the Chinese administration is not loathe to deploying economic means – or sanctions of another kind – to safeguard what it perceives as its strategic interests. Indeed, Beijing wields its control over critical raw materials as a tool of strategic and political leverage, as evidenced by its extending export restrictions over gallium and germanium (impacting semiconductors) in October to graphite products, which are crucial for the lithium-ion batteries of electric vehicles.

Europe clearly does and should exercise strategic agency in balancing the needs to advance climate sustainability and to uphold domestic interests. Yet the proverbial ‘Devil’ lies in the details. Whether Beijing acts upon its strongly worded messages towards the EU, will depend on the impact and stringency of the measures ensuing the investigation, as well as China’s broader strategic objectives.

European leaders must evaluate the impact of potential Chinese bans on European vehicles and companies on the deindustrialisation of Europe. Their priorities should be placed on strengthening the EV industrial strategy instead of jeopardising affordable EV market options, thereby complicating the green transition. Europe should hence approach relations with China judiciously, aiming to prevent further tensions, while capitalising on diversifying beyond both the U.S. and China.

Amidst the challenges posed by Chinese innovation, the forthcoming Commission must prioritise aligning and calibrating more comprehensively the EU’s industrial and investment strategies. This entails focusing on enhancing EV technology, fostering green innovation, and promoting environmental excellence rather than protectionism. Furthermore, actions such as those outlined in the Critical Raw Materials Act, responsible de-risking, and revising state aid prohibitions, would be crucial for enhancing the EU’s global competitiveness in the EV and automobile industries.