We are living in a very different world. Shifting macroeconomic trends including diversification and second sourcing because of de-globalization and de-coupling have significant implications for the global economy. The strategic competition between the United States and China and other major geopolitical developments will fundamentally shape the world we live in.

Global Economic Trends

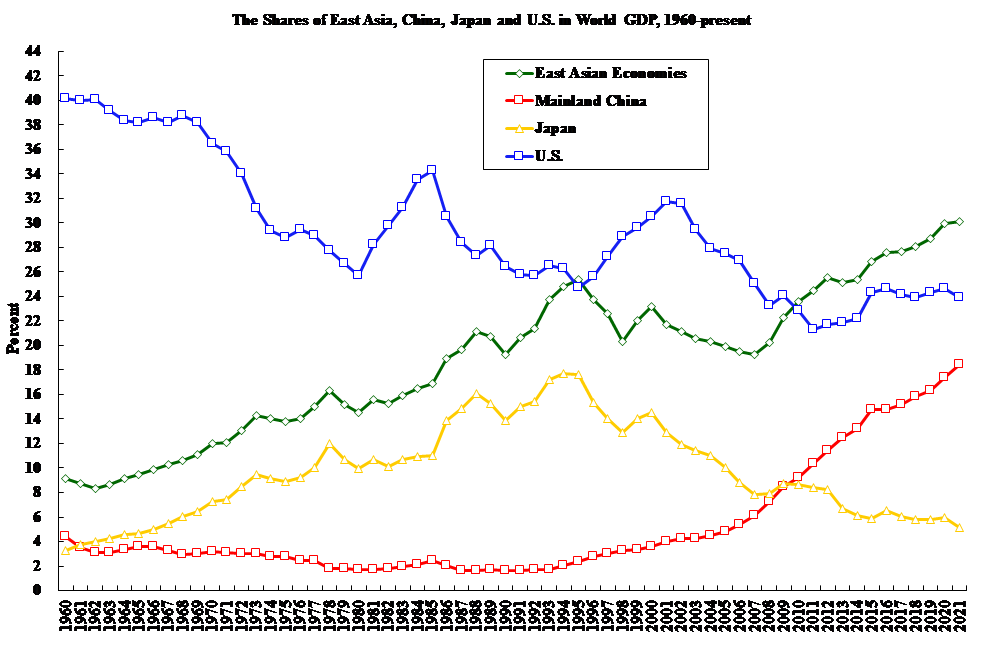

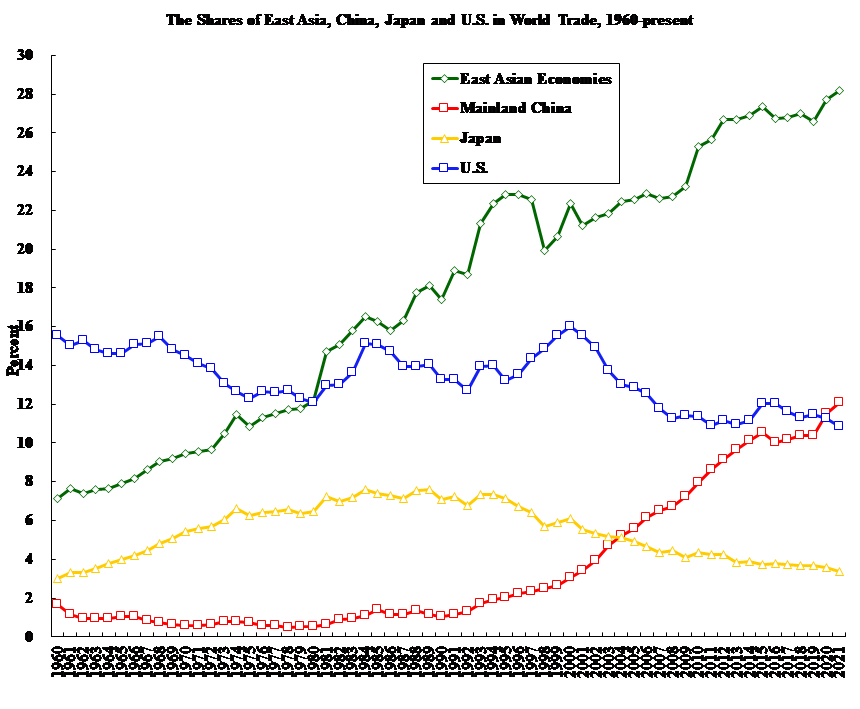

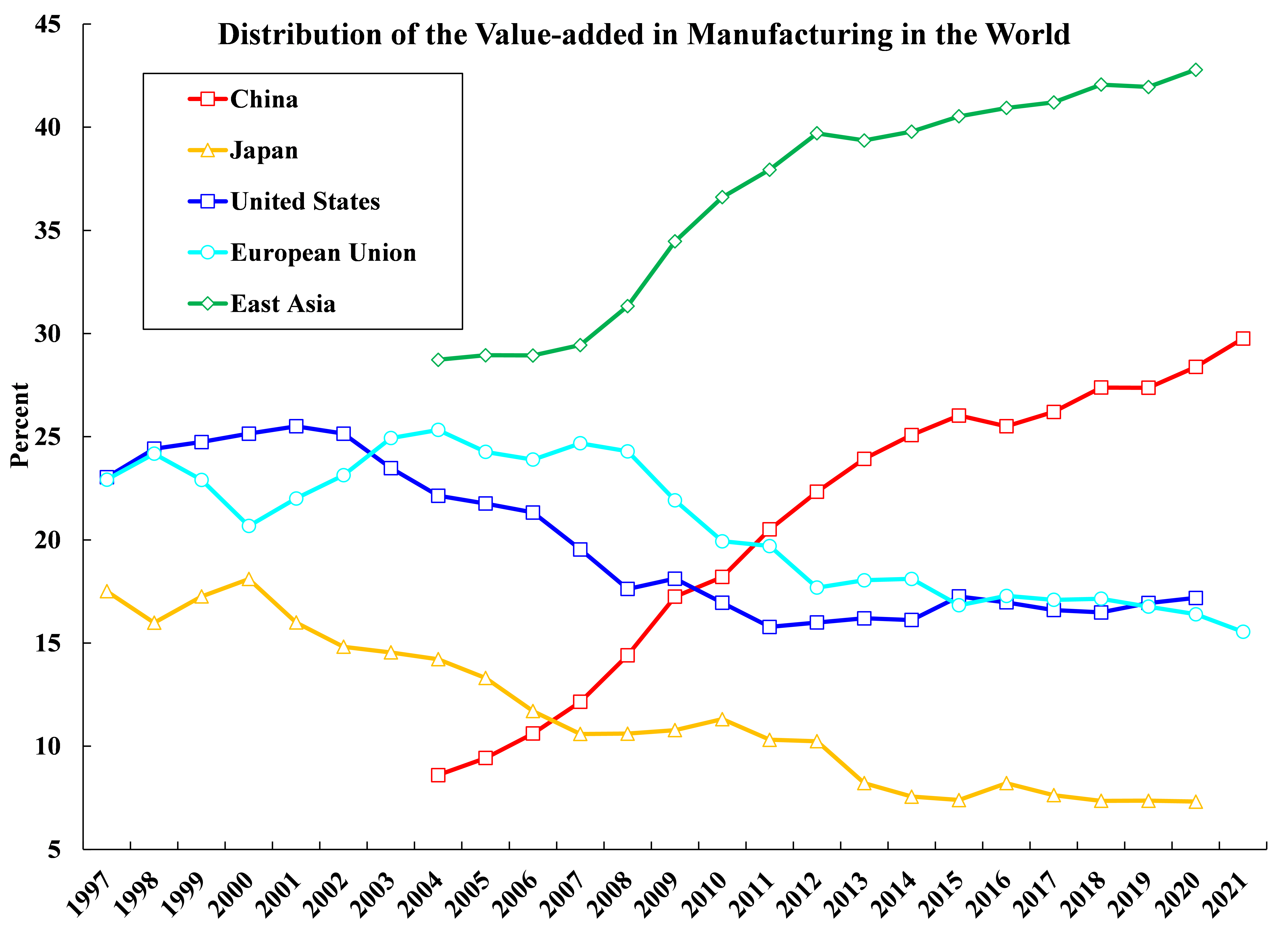

The center of gravity of the world economy has been shifting from North America and Europe to East Asia since 1960, and within East Asia from Japan to China beginning in the mid-1990s. And this has been happening in real GDP, international trade, wealth, manufacturing, and innovation.

First, wealth. From various reported surveys, there are supposedly more than six hundred known US$ billionaires in China, possibly more than in the United States. There may be many more unknown ones in China. (The counts vary across different surveys but the orders of magnitudes of the numbers of billionaires in both countries are the same.) The aggregate wealth of Chinese households has also been rising rapidly.

China is considered a manufacturing powerhouse. Over the past decades, many successful Chinese enterprises, both state-owned and private, have emerged. The 2022 Fortune Global 500 list includes 145 Chinese enterprises, compared to 124 U.S. enterprises. Many of the Chinese enterprises are engaged in manufacturing. Collectively, the revenue of the Chinese enterprises on the list exceeded the revenue of the U.S. enterprises for the first time.

On the Verge of a Breakthrough in Innovation and Technology

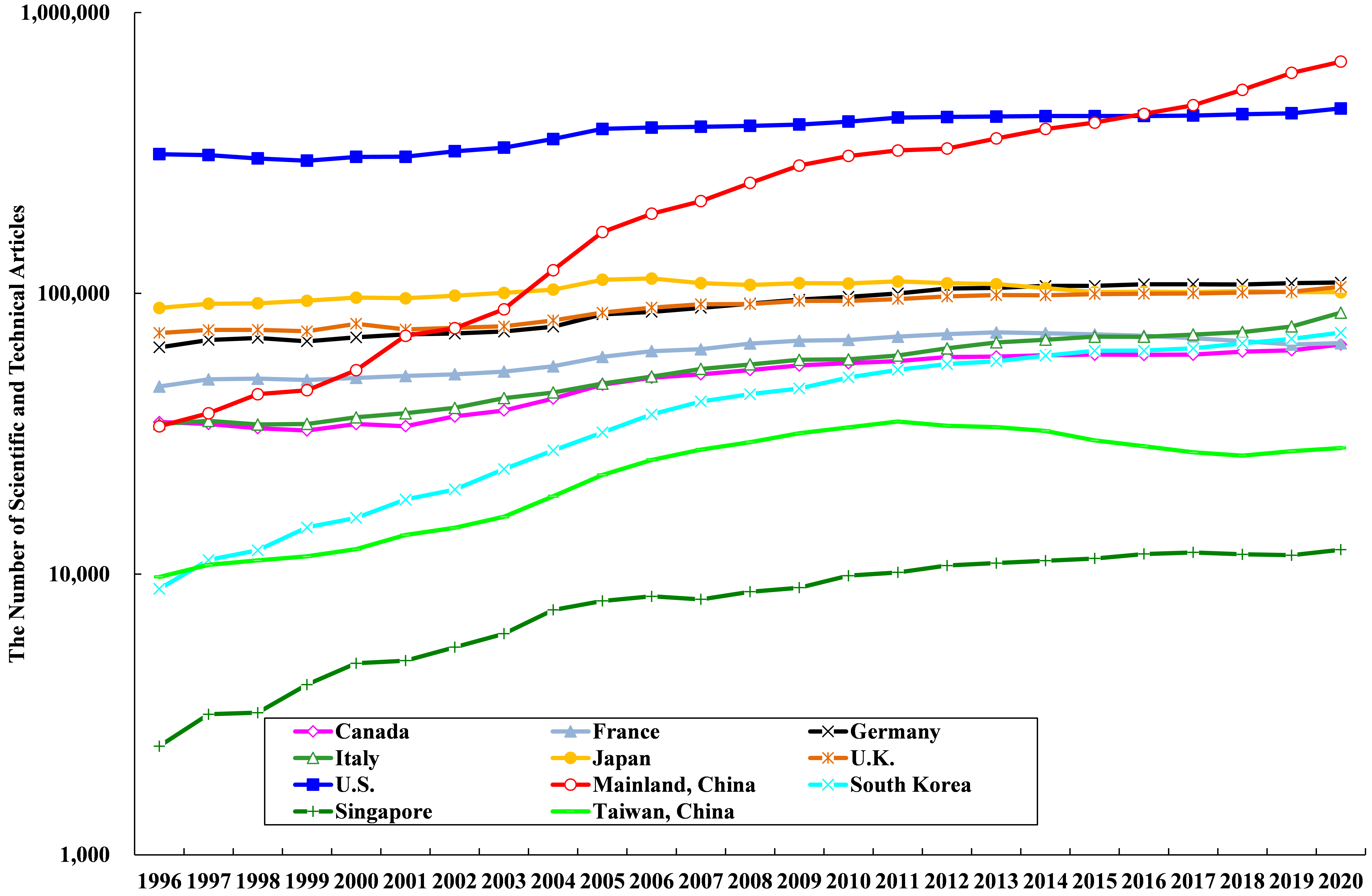

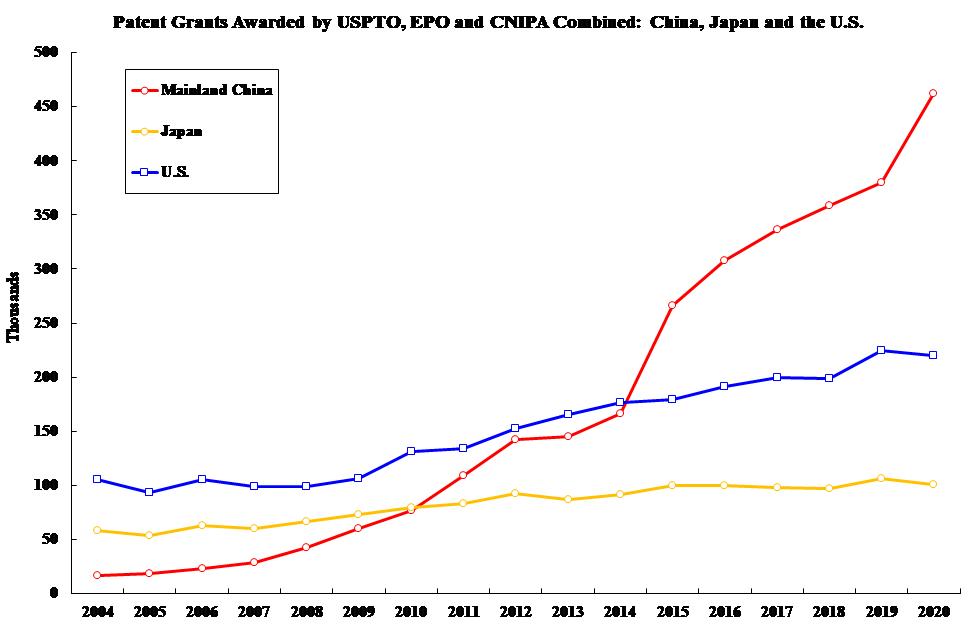

In terms of innovation, China has greatly strengthened its intellectual property protection since 2014. It has also been increasing its investment in research and development (R&D), which reached 2.44% of GDP in 2021. China has recently become the top country in terms of the total number of scientific and engineering articles published in international professional journals by its nationals, the total number of their citations, and the total number of the top 1% of most frequently cited articles. Furthermore, China was awarded the largest number of patents in 2021 by the U.S. Patent and Trademark Office, the European Patent Office and the China National Intellectual Property Administration combined, followed by the U.S. and Japan.

The Number of Scientific and Engineering Articles by Authors of Countries

According to the Top500 list of super-computers in the world, ranked by speed, published in June 2022, 173 were in China, 127 were in the U.S. and 34 were in Japan. The fastest supercomputer is currently the U.S.’s Frontier, located at Oak Ridge, Tennessee. However, it was acknowledged that a couple of Chinese super-computers, Sunway Ocean Light (神威海洋之光)and Tianhe III (天河三號), which did not participate in the ranking exercise, may be even faster. These two Chinese super-computers have supposedly been built with only Chinese components and parts.

China is on the verge of a breakthrough in innovation and technology. Indigenous innovation has been occurring in many areas, for example: 5G communication, the BeiDou Navigation Satellite System, high-speed trains, quantum communication, super-computers, and ultra-high-voltage transmission of electricity. The vast Chinese market attracts entrepreneurs, innovators, and venture capitalists because of its economies of scale. There will be many start-ups in China, and many failures resulting therefrom, but a small number will manage to become “unicorns”.

Internationalization of Renminbi

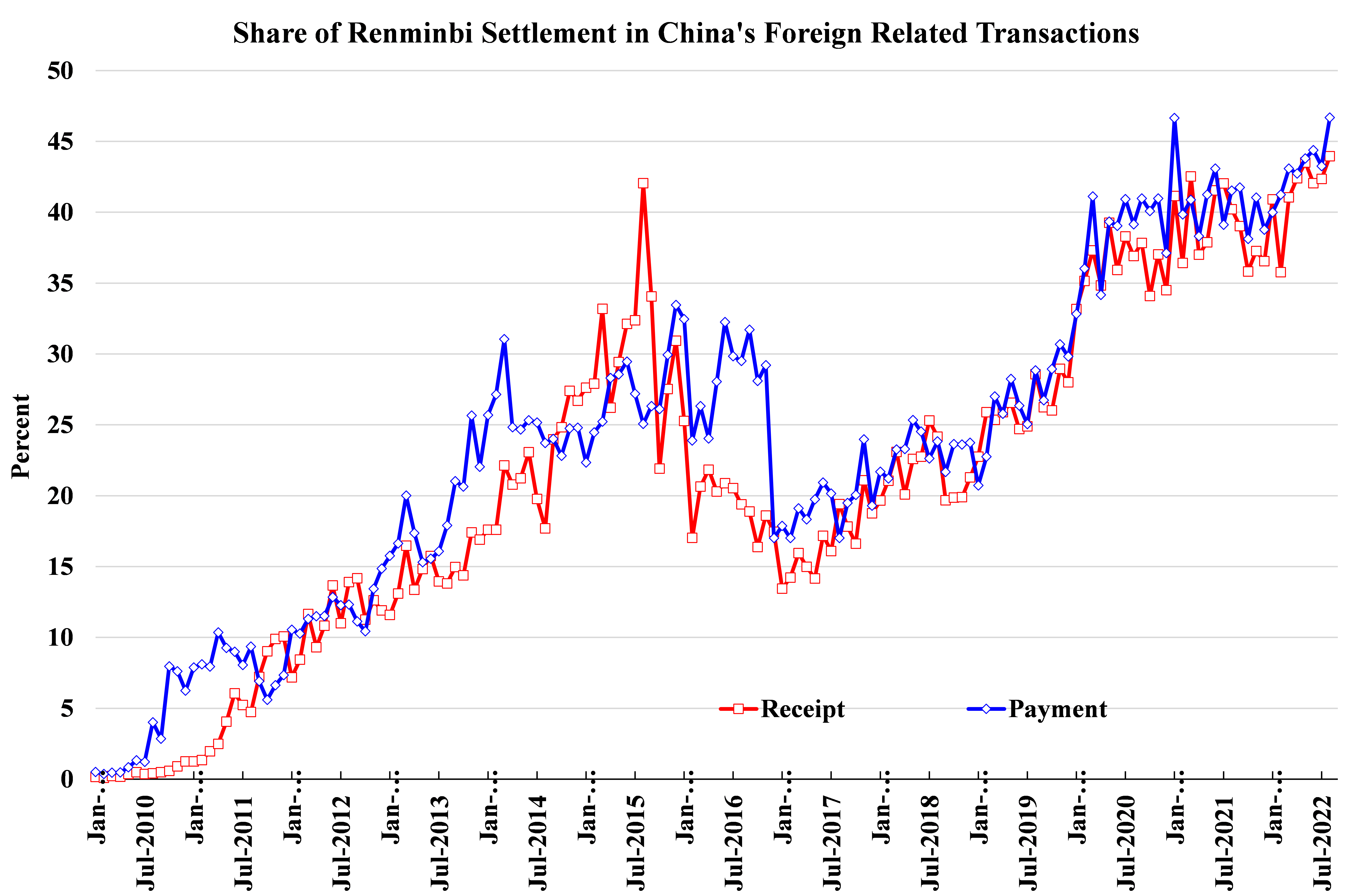

Another notable macroeconomic trend is the RMB internationalization. The Renminbi has been current-account convertible since 1994. Its value rests on the purchasing power of the Renminbi for Chinese goods and services (and assets). For all practical purposes, the offshore Renminbi is completely convertible in Hong Kong. The Chinese capital control applies only to certain capital flows into and out of the Mainland.

Own-currency settlement of bilateral transactions between two countries, as opposed to settlement in a third-country currency, actually reduces both transaction costs and exchange rate risks for both countries. It requires only one currency exchange, and incurs only one exchange rate risk, and can hence benefit both countries. If a third-country currency is used for settlement, it will require two currency exchanges, doubling the transaction costs, and be subject to two exchange rate risks. More and more countries have entered into own-currency settlement agreements with China, for example, Indonesia and Russia, settling their international economic transactions with China in Renminbi and their own currencies, the Rupiah and the Ruble.

The weaponization of the Society for Worldwide Interbank Financial Telecommunication (SWIFT) system for international payments in US dollars has forced countries to seek alternatives. The use of the U.S. Dollar as an international medium of exchange and store of value will be undergoing a gradual decline.

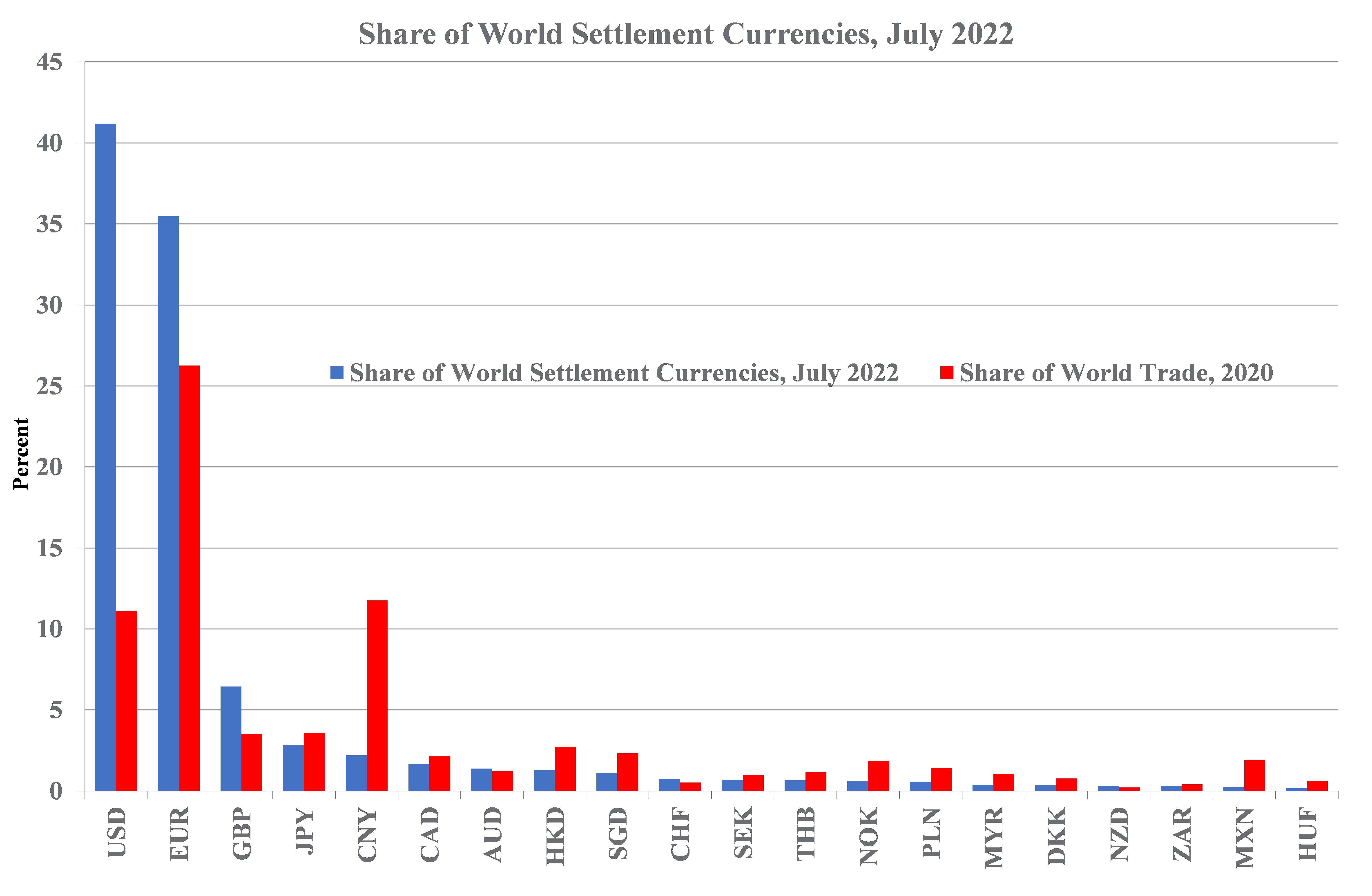

If China can achieve the same share of world settlement in its Renminbi as Japan in its Yen relative to its share in world trade, the share of Renminbi in world settlement will rise from its current 2.2% to 9.2% and will become the third most widely used settlement currency in the world. Initially, this will be driven by own-currency settlement of Chinese international trade transactions with its trading-partner countries.

Even at 9.2%, the Renminbi will still be dwarfed by the over 40% share of the U.S. Dollar in world settlement. However, it is probably not in the national interests of China for the Renminbi to aspire to replace the U.S. Dollar as the international medium of exchange. Instead, China should promote the settlement of bilateral trade transactions in the own currencies of the two trading-partner countries, which was the practice under the old Bretton-Woods arrangement.

The world continues to witness de-globalization and de-coupling. Just as economic globalization increases the welfare of all countries in the world, economic de-globalization decreases the welfare of all countries. Economic de-globalization and de-coupling reduce the choice sets facing every economy, result in a decline in welfare for everyone, and slow down global economic growth.

De-coupling of economies is likely to result in temporary disruptions of the existing supply chains, affecting production around the world. Multiple, parallel, independent trading blocs as well as supply chains will emerge. There will be a resurgence of protectionism worldwide, in the forms of import barriers and export controls.

De-coupling of the Chinese and U.S. economies in some form appears inevitable, not only because of the COVID-19 epidemic and the possibility of the emergence of other viruses in the future, but also because of the increasing strategic competition between the two countries.

Diversification

Both the COVID-19 pandemic and the Russia-Ukraine conflict demonstrate the potential benefits of diversification as insurance against the disruption of supply chains. For example, some European economies should probably have had more diverse sources of supply of oil and natural gas. Some of them have been relying predominantly on Russia. China, which imports the bulk of its oil and natural gas, is appropriately diversified by country (for example, Angola, Russia, Saudi Arabia, and the United States) and by transportation route.

A prerequisite for diversification is the availability of at least a sustainable second source of supply. Second sourcing means finding an alternate source of long-term supply for a product or a service, either domestically or through imports from a third country. Second-sourcing is a natural response to the potential disruption of a supply chain. With a second source of supply, the economy is basically protected from the disturbances resulting from unexpected events such as various kinds of natural disasters (earthquakes, tornadoes, tsunamis, and volcanic eruptions), epidemics such as the COVID-19, wars, revolutions, and other geo-political conflicts. Second-sourcing is like purchasing insurance, but insurance that is more durable.

Multiple Supply Chains

The most likely long-term outcome of economic de-coupling is the emergence of two or more efficient supply chains for every product and service in the world. The world market is large enough to accommodate more than one or even two efficient global supply chains for any product or service.

The existence of multiple supply chains is potentially a positive development for the world economy because it reduces monopoly power, enhances competition, and protects the world from the risks of catastrophic total system failures. It should also eventually result in a lower price and a higher quality for the product or service.

The world economy will be better off in the long run because of the increase in resilience and stability. For example, it is probably beneficial for the world to have one or more viable alternative cross-border payment systems in addition to SWIFT so that they will not be weaponized.

The COVID-19 Epidemic

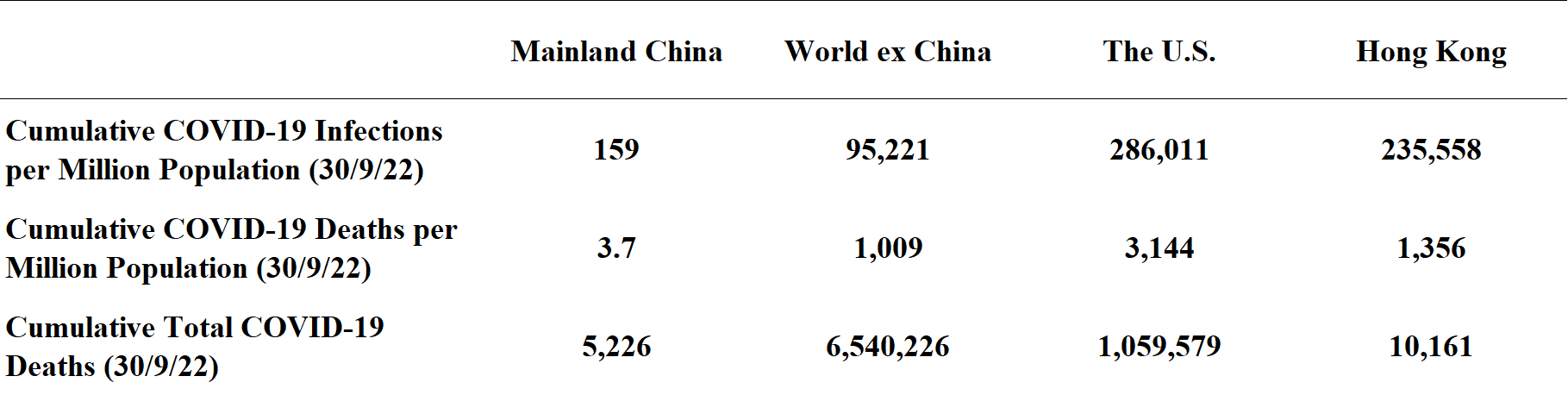

The COVID-19 epidemic, which broke out in Hubei, China, in late 2019, is unfortunately still on-going. However, the Mainland has done very well in containing the COVID-19 epidemic, even though it first broke out there.

If the Mainland were to have the same death rate as the U.S., the cumulative total deaths as of 30/9/2022 would have increased from 5,226 to 4.5 million.

As a result of the COVID-19 pandemic, the cumulative rate of growth of real GDP over the ten quarters since 2020 on the Mainland has been reduced by 7.5%, from 16.3% to 8.8%, compared to the ten quarters before. For the U.S., the reduction has been only 4.2%, from 6.7% to 2.5%. There appears to be a trade-off between the reduction in the growth of GDP and the COVID-19 cumulative death rate. A lower reduction in the GDP growth rate is associated with a higher cumulative death rate.

The World and Its Major Economies

The latest published forecasts of annual rates of growth of real GDP by international organizations indicate that the whole world economy is slowing down except for India.

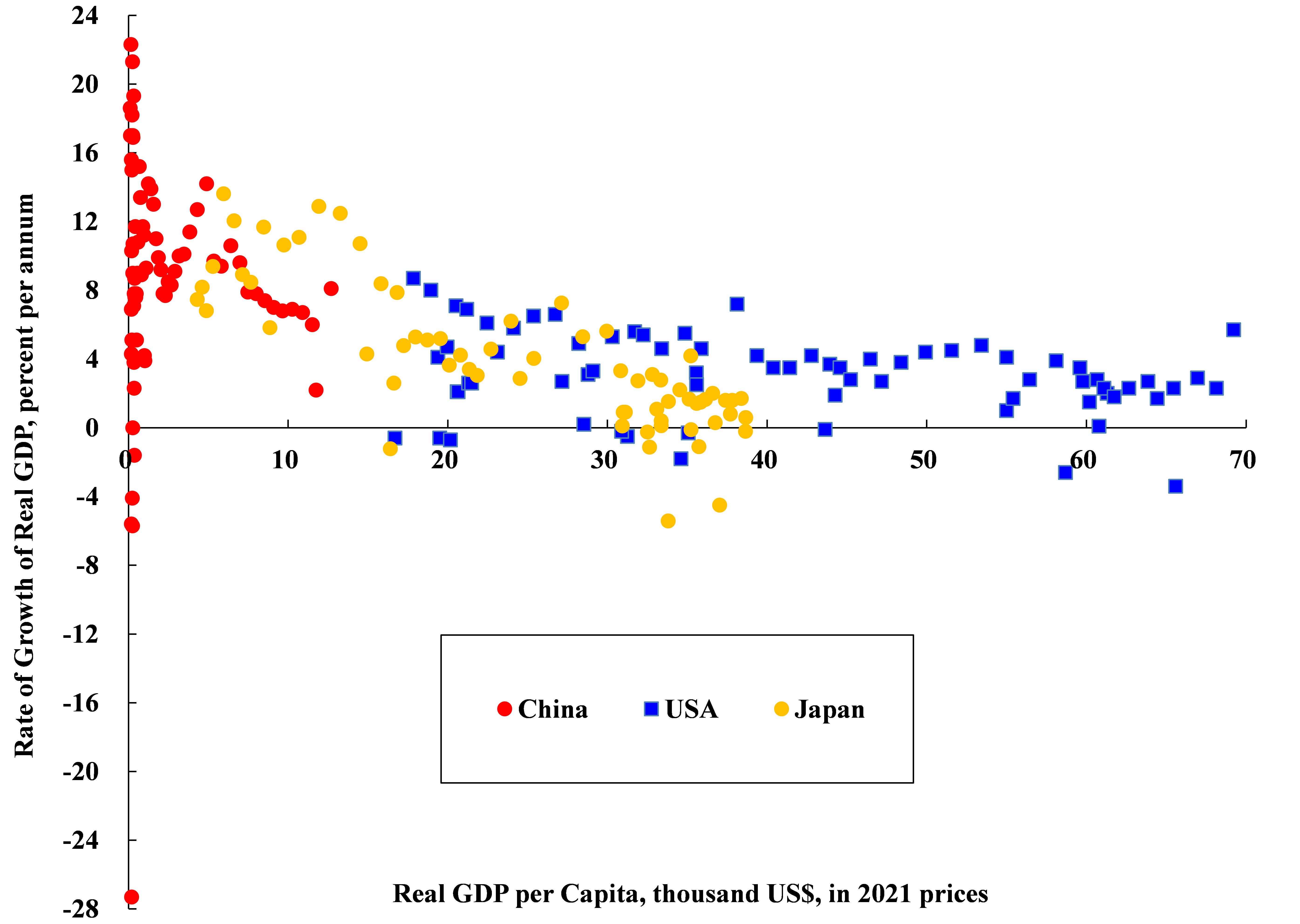

The Chinese Economy

The Chinese economy will be growing faster than those of North America and Europe in the next decade even though all of them will be slowing down.

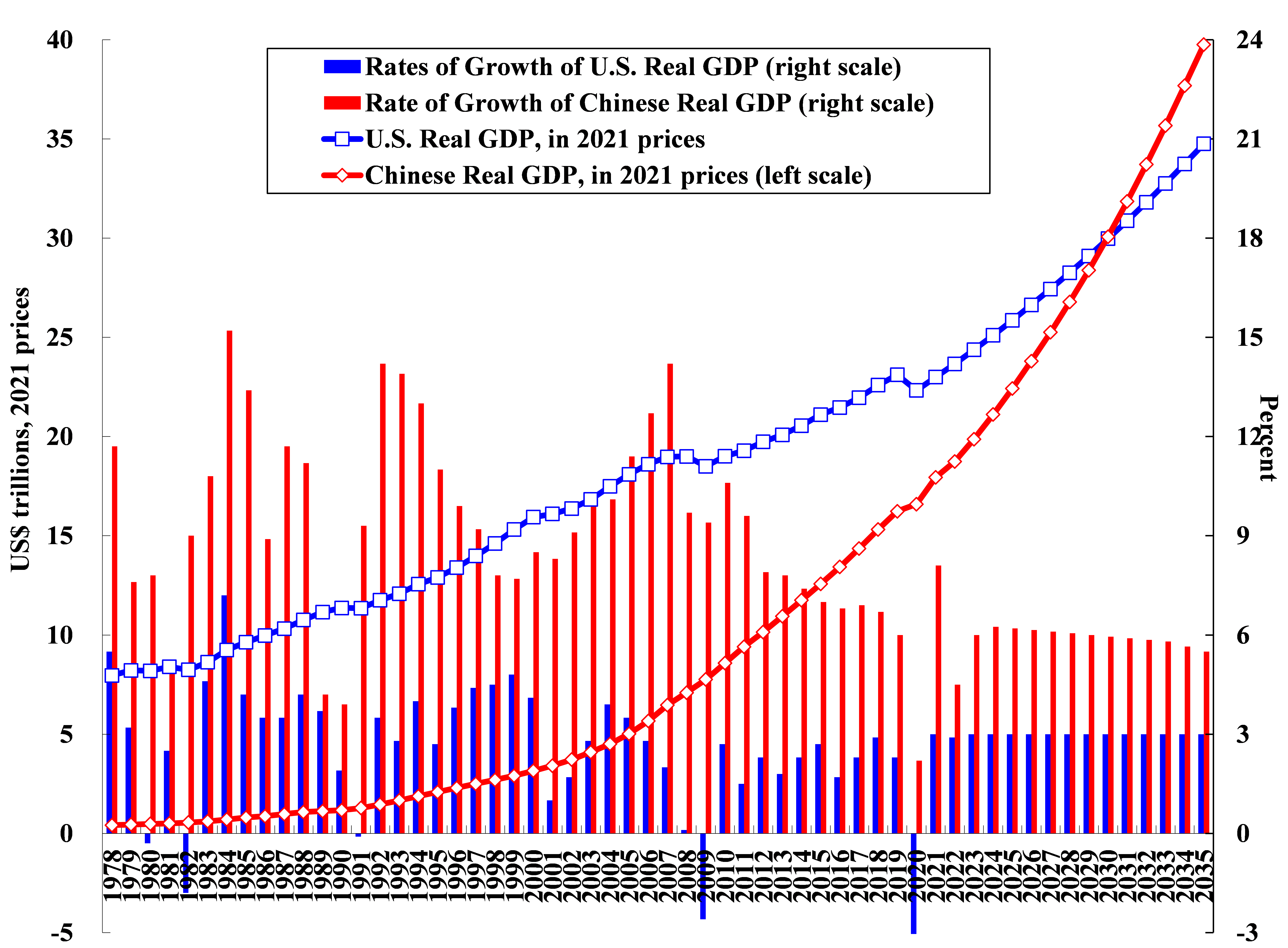

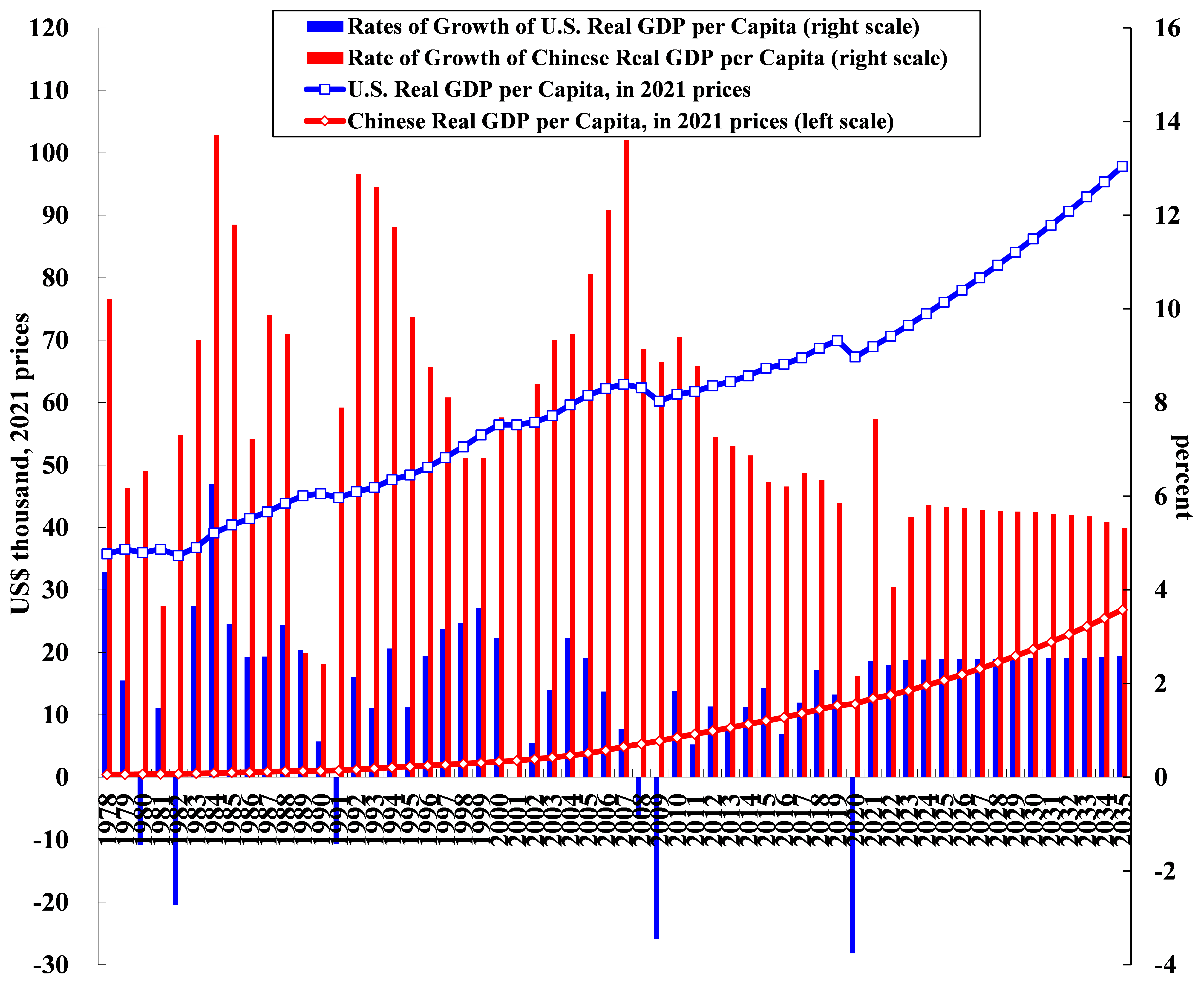

There is an empirical regularity that as the real GDP per capita of an economy rises, its real rate of growth falls. The Chinese economy cannot continue to grow at a real rate of 9-10% per annum as it did between 1978 and 2018, but its real GDP per capita is still in a range that would allow its economy to grow at an average annual real rate of approximately 6%. My forecast is that by 2030, the real GDP of Mainland China at market prices will reach parity with that of the U.S., at approximately US$30 trillion, in 2021 prices.

With an annual rate of growth in real GDP of 6% on average and a national savings rate more than 40%, the wealth of Chinese households and institutions will also grow by leaps and bounds. It is this wealth that will drive the Chinese demand for physical and financial assets, domestically, as well as abroad, because of the need for diversification.

Comparison of Actual and Projected Chinese and U.S. GDPs

Comparison of Actual and Projected Chinese and U.S. GDPs per Capita

Implication for Hong Kong

As for Hong Kong, its economy will do reasonably well if the Chinese economy does well. The more widespread use of the Renminbi offshore is beneficial to Hong Kong as the premiere centre for offshore Renminbi. For example, it can help other countries raised funds in Hong Kong through Renminbi-denominated bonds, which can be used to pay Chinese suppliers for their infrastructural projects (equipment and contractors).

Hong Kong can play a valuable intermediary role as the overseas Chinese communities in the ASEAN countries re-establish their historic connections to their home regions on the mainland. There is a great deal of room for Hong Kong to use fiscal policy to stimulate its economy. It has large fiscal reserves and almost no public debt. Fundamentally, it has to increase employment, but the financial sector can provide only limited opportunities for additional employment, so Hong Kong must develop new sources of aggregate demands. For example: retrofitting public buildings to be more energy-efficient; digitisation of all documents; etc.

China-U.S. Strategic Competition

The U. S. ruling elite including the military-industrial complex wants to maintain its global hegemony, or primacy, in the name of preserving a rules-based international order. It wants to perpetuate the so-called “Pax Americana (American Peace)”. The objective of the U.S. ruling elite is to prevent the rise of a country which can potentially say no to the U.S., using all means available. If any country is allowed to get away with saying no to the U.S., other countries may be tempted to follow suit, and the U.S. global hegemony may soon be no more.

China is not really a threat to the existence and continued prosperity of the U.S. and will never be one. However, China may be a threat to the continued global hegemony of the U.S. because China can say no to the U.S., just like the former Soviet Union.

If the U.S. loses its global hegemony, the predominance of the U.S. Dollar as an international medium of exchange and store of value may also be threatened. This will be a seriously negative development for the U.S. economy as it will no longer be able to run large trade deficits indefinitely by simply printing and selling U.S. Government bonds. The U.S. will therefore try to do all it can to maintain its global hegemonic position. Thus, China-U.S. strategic competition will likely be the new normal in the coming decade.

The U.S. strategy is essentially one of containment (pivot to Asia, TPP, the QUAD (consisting of Australia, India, Japan, and the U.S.), and the AUKUS (Australia, the U.K., and the U.S.). The United States uses a trade, technology, and currency war (tariff and non-tariff barriers, restrictions on high-technology trade, and possible restrictions on the use of the USD payment system), as well as a propaganda war to demonize China about Hong Kong, Tibet, and Xinjiang.

It is tempted to provoke China to fire the first shot across the Taiwan Straits to create a pretext for organizing international sanctions against China. If there is going to be a war between China and the U.S., the sooner is probably the better for the U.S. However, even better for the U.S. is a proxy war between the Mainland and Taiwan, without involving U.S. “boots on the ground”.

China’s Objectives and Strategy

The Chinese objectives stand in sharp contrast. For China, it is all about peaceful development. Chinese real GDP per capita is still at a relatively low level by world standards. China needs to raise its real GDP per capita, which is currently less than one quarter of that of the U.S., much more. China did not initiate the strategic competition or the trade and technology wars with the U.S. Its intension is to ensuring survival and continual development and growth of the nation with a stated goal of rejuvenation of the Chinese nation. To achieve the objectives, China intends to build new-type of relations with other major powers based on the principles of mutual respect, trust, and non-interference; peaceful co-existence, and win-win cooperation, and focuses on building a global community of shared future, which means seeking cooperative solutions to global problems such as climate change and pandemic.

China maintains a credible second-strike deterrent capability with a “no first use” policy for nuclear weapons. To counter efforts to contain China, the Chinese government is getting prepared for possible de-coupling by developing self-reliant survival-critical systems (e.g., the BeiDou Navigation Satellite System), promoting indigenous innovation and creating alternative cross-border payment systems such as the Cross-border Interbank Payment System (CIPS). In addition, China maintains an open economy for trade and investment to all friendly countries.

Potential Flash Points

There are a few potential flash points including the South China Sea, the East China Sea, the Taiwan Straits, and all-out rivalry that could drag China and the U.S. into a so-called the Thucydides trap.

It is likely that China will be able to reach an accommodation with most of the ASEAN countries, being the most important trading-partner country for almost all of them. Joint economic development with shared benefits can be a viable long-term solution. China has little or no incentive to interrupt the freedom of navigation on one of its most important sea routes. On the contrary, it is concerned about potential interruption by outside naval powers.

The conflict in the East China Sea is mostly focused on the Diaoyu Islands, which historically were administered as part of Yilan Xian of the Province of Taiwan. It is unlikely to trigger a full-scale war. As long as Japan is unable to become a “normal” country, that is, to have its own independent national defense, it will have to continue to be a “protectorate” of the U.S. and take orders from it. Japan can have an independent foreign policy only when it is able to defend itself independently.

In 1989, Shintaro Ishihara, a former Governor of Tokyo, and Akio Morita, the co-founder and former Chairman of SONY, co-authored "The Japan That Can Say No: Why Japan Will Be First Among Equals “. However, the truth is that Japan is still unwilling and unable to say no to the U.S. even today. Japan is probably the most sensitive about the reunification of the Mainland and Taiwan as it will make the Taiwan Straits a Chinese inland sea. At the present time, most of Japanese trade with Southeast Asia, South Asia, the Middle East, and Europe is routed through the Taiwan Straits. In principle, the Northern Passage to Europe is potentially possible, but Russia will have control over that route. But as long as peace prevails, there is little incentive for anyone to interrupt the maritime traffic.

The reunification of Taiwan with the Mainland is, like the reversion to Chinese sovereignty of Hong Kong and Macau, a matter of Chinese national honor. Taiwan to China is like Alsace-Lorraine to France, Goa and Pondicherry to India, and the four Northern Islands to Japan. Reunification will be pursued by any Chinese central government with the ability to do so, regardless of its ideology or whether it is popularly elected. People on both sides of the Taiwan Straits will benefit enormously from a peaceful reunification and should therefore work hard to achieve it. The rest of the world will benefit greatly too. With peaceful reunification, a large number of lives will be saved, enormous destruction will be avoided, and huge peace dividends will be available to be shared by all. The use of force is only a very last resort.

The Thucydides’ Trap

Despite the tense relations, the China-U.S. strategic competition is unlikely to result in a hot war between the two countries because such a war will have no winners, only losers. And the leaders on both sides know that. If the U.S. and the former Soviet Union did not go to war in the last century, there is even less reason for China and the U.S. to go to war in this century, notwithstanding the so-called “Thucydides’ trap”. For both countries, “Mutually Assured Destruction” remains the foundation of “peace”.

The on-going Russia-Ukraine is one of the greatest geopolitical challenges we are witnessing. Can the war be contained? Can it be sustained? Is a cease-fire possible? Those questions remain unanswered.

The changing global landscape and the China-U.S. strategic competition pose challenges to Hong Kong. Hong Kong should have little illusion that it can or will be treated differently from the rest of China by the U.S. and its allies, so long as the China-U.S. strategic competition is the new normal. It is in Hong Kong’s interests to encourage the active use of the Renminbi in Hong Kong in parallel with the Hong Kong Dollar (even though the HKD remains the sole legal tender). The introduction of central bank digital currencies (CBDCs) such as e-CNY and e-HKD will facilitate the parallel circulation of the Hong Kong Dollar and the Yuan in the Guangdong-Hong Kong-Macau Greater Bay Area. The financial institutions in Hong Kong should subscribe to multiple cross-border payment systems, including the Cross-border Inter-bank Payment System (CIPS) introduced by the People’s Bank of China. This will assure that international payment transfers to and from Hong Kong can continue uninterrupted even if the SWIFT system is no longer available to Hong Kong financial institutions.

To sum it up, the world economy will probably go into a recession. It is unlikely to resume its robust growth until the resolution of the Russia-Ukraine conflict, even though the setbacks caused by the COVID-19 epidemic and the inevitable de-coupling of the economies are temporary. The de-coupling and the emergence of alternative supply chains and second sources should reduce the market power of monopolies and enhance the economic and financial stability and resilience of the world. It will also make weaponization of economic instruments meaningless. With two or more sources for each product, service and supply chain, the world is also protected from the possibility of a catastrophic total system failure, from natural or man-made disasters. The China-U.S. strategic competition may not end with a clear outcome. At some point, the U.S. may realise that it is futile to try to prevent China’s rise and that China is not an existential threat to it. Then the two countries may be able to reach a detente.